When deciding between a HELOC and a home equity loan for renovation projects, understanding the key differences is crucial. This article delves into the advantages and disadvantages of each option, helping you make an informed choice that suits your financial needs.

HELOC vs. Home Equity Loan

When considering renovations, it's important to understand the key differences between a Home Equity Line of Credit (HELOC) and a Home Equity Loan. Both options allow you to borrow against the equity in your home, but they have distinct features that may make one more suitable than the other for your renovation project.Benefits of Choosing a HELOC

A HELOC provides a flexible line of credit that allows you to borrow funds as needed, similar to a credit card. This can be advantageous for renovation projects where costs may vary or if you prefer to have access to funds over a period of time.

Additionally, with a HELOC, you only pay interest on the amount you borrow, giving you the ability to manage your expenses more efficiently.

Advantages and Disadvantages of Home Equity Loan

On the other hand, a Home Equity Loan provides a lump sum upfront, which may be beneficial if you have a clear renovation budget in mind. This type of loan typically offers a fixed interest rate, making it easier to predict monthly payments.

However, with a Home Equity Loan, you will be charged interest on the entire loan amount, regardless of how much you actually use for renovations. This could result in higher overall costs compared to a HELOC.

Flexibility of Funds and Repayment Terms

A HELOC offers more flexibility in terms of accessing funds and repayment. You can borrow, repay, and borrow again within the specified draw period, usually around 10 years. This flexibility can be beneficial for ongoing renovation projects or unforeseen expenses.

Moreover, HELOCs often come with variable interest rates, which can be advantageous if rates are low but may pose a risk if rates increase over time. Home Equity Loans, on the other hand, typically have fixed rates, providing stability in repayment amounts.

Qualifying and Application Process

When it comes to getting a HELOC or a home equity loan for renovations, understanding the qualification requirements and application process is crucial to securing the right type of financing.Qualification Requirements

- HELOC: To qualify for a HELOC, lenders typically look for a strong credit score, usually above 700, a low debt-to-income ratio, and a good amount of equity in your home. Some lenders may also require a minimum amount of home equity, such as 15% or 20%.

- Home Equity Loan: Similar to a HELOC, a home equity loan requires a good credit score, typically in the mid-600s or higher, a low debt-to-income ratio, and a significant amount of equity in your home. Lenders may also have specific requirements for the minimum amount of equity needed.

Application Process

- HELOC: The application process for a HELOC involves filling out an application with the lender, providing documentation of your income, assets, and debts, and undergoing a credit check. Once approved, you can access funds as needed up to your credit limit.

- Home Equity Loan: Applying for a home equity loan requires similar documentation and credit checks as a HELOC. However, instead of a revolving line of credit, you'll receive a lump sum of money upfront, which you'll repay over a set term with fixed monthly payments.

Role of Credit Scores and Equity

- Both HELOCs and home equity loans heavily rely on your credit score to determine your eligibility and the terms of the loan. A higher credit score can help you secure better interest rates and loan terms.

- Equity in your home is also a crucial factor in the approval process. Lenders want to ensure that you have enough equity in your home to cover the loan amount and mitigate their risk.

Tip: To improve your credit score and increase your chances of getting favorable terms for a HELOC or home equity loan, focus on paying down existing debts, making timely payments, and avoiding taking on new debt before applying for a loan.

Interest Rates and Fees

When considering financing options for renovations, it is crucial to understand the interest rates and fees associated with HELOCs and home equity loans. These factors can greatly impact the overall cost of borrowing and should be carefully evaluated before making a decision.Interest Rates

- HELOCs typically have variable interest rates, which are tied to the prime rate. This means that your interest rate can fluctuate over time, potentially leading to higher payments.

- Home equity loans, on the other hand, usually come with fixed interest rates. This provides more stability and predictability in your monthly payments, as the rate remains constant throughout the loan term.

- Interest rates for both HELOCs and home equity loans are generally lower than other forms of borrowing, such as credit cards or personal loans, due to the collateral involved (your home's equity).

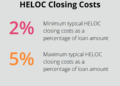

Fees

- When obtaining a HELOC, you may encounter fees such as application fees, annual fees, closing costs, and early closure fees. These fees can add up and impact the overall cost of borrowing.

- Home equity loans also come with fees, including closing costs, appraisal fees, origination fees, and prepayment penalties. It's important to factor in these fees when comparing loan options.

- Some lenders may offer promotions or incentives to waive certain fees or provide discounts on closing costs. It's worth exploring these options and negotiating with lenders to reduce fees.

Considerations for Loan Repayment

:max_bytes(150000):strip_icc()/dotdash-home-equity-vs-heloc-final-866a2763fd0548eaa393afa0ffd7372b.jpg "Home Equity Loan vs. HELOC: What’s the Difference?") When it comes to financing home renovations with a HELOC or a home equity loan, understanding the repayment options and potential risks is crucial to avoid financial pitfalls in the future.

When it comes to financing home renovations with a HELOC or a home equity loan, understanding the repayment options and potential risks is crucial to avoid financial pitfalls in the future.Repayment Options

- HELOCs typically have a draw period during which you can access funds and make interest-only payments. After the draw period ends, you enter the repayment period where you must pay back both the principal and interest.

- Home equity loans, on the other hand, involve fixed monthly payments over a set term, similar to a traditional mortgage.

Risks of Using a HELOC or Home Equity Loan

- One risk of using a home equity loan or a HELOC for renovations is the potential to overextend yourself financially, leading to difficulty in making payments.

- If the value of your home decreases, you may end up owing more than your home is worth, known as being "underwater" on your mortgage.

Effective Budgeting for Loan Repayment

- Create a detailed renovation budget to understand exactly how much you need to borrow and how it aligns with your financial situation.

- Factor in potential interest rate increases when budgeting for loan repayment to ensure you can afford higher payments in the future.

- Consider setting aside an emergency fund to cover unexpected expenses or financial setbacks that could impact your ability to make loan payments.

Avoiding Default and Consequences

- Missing payments on a HELOC or a home equity loan can damage your credit score and put your home at risk of foreclosure.

- Communicate with your lender if you anticipate difficulty in making payments to explore alternative repayment options or seek financial assistance.

Conclusive Thoughts

In conclusion, weighing the benefits of a HELOC versus a home equity loan for renovations involves careful consideration of factors like flexibility, interest rates, and repayment terms. By assessing your specific requirements and financial goals, you can choose the option that aligns best with your renovation plans.

Answers to Common Questions

What are the key differences between a HELOC and a home equity loan?

A HELOC operates as a revolving line of credit, while a home equity loan provides a lump sum amount.

How can I improve my credit score to secure better terms for a HELOC or home equity loan?

To enhance your credit score, focus on making timely payments, reducing debt, and checking your credit report for errors.

Continue this structure for all FAQs